· Guide · ![]() Yanko · 3 min read

Yanko · 3 min read

Save First Then You Can Start Spending

Your complete guide to the Pay Yourself First method that makes 50/30/20 even better

You know the pattern: You plan to save money this month. You pay your rent, groceries, bills. Maybe grab coffee a few times. Buy that thing on Amazon. And at the end of the month… there’s $47 left. Better than nothing, right?

Except next month, there’s $12. The month after? You actually overdrafted.

This is why traditional budgeting has a 80% failure rate. When savings comes last, life always finds a way to eat it.

Enter: Pay Yourself First

The concept is simple but counter-intuitive: Save money before you spend it, not after.

When my wife and I were using the 50/30/20 budgeting method (50% needs, 30% wants, 20% savings), we kept falling short on that 20%. We’d hit 12%, maybe 15%, but rarely the full amount. We knew what we should save. We just couldn’t make it happen consistently.

Then we discovered Pay Yourself First and flipped the script: The moment income hits our account, 20% goes to savings. Automatically. Before we see it. Before we spend it. Before we can talk ourselves out of it.

It worked. Suddenly we were consistently hitting our savings targets.

But then we realized something even more important…

Not all savings are created equal.

Some savings are urgent: emergency fund refills, retirement investments, insurance premiums. Others are important but flexible: vacation funds, celebration money, wish-list items.

We were treating a $2,000 emergency fund gap the same as $2,000 for a beach vacation. That didn’t feel right.

So we created a tiered system:

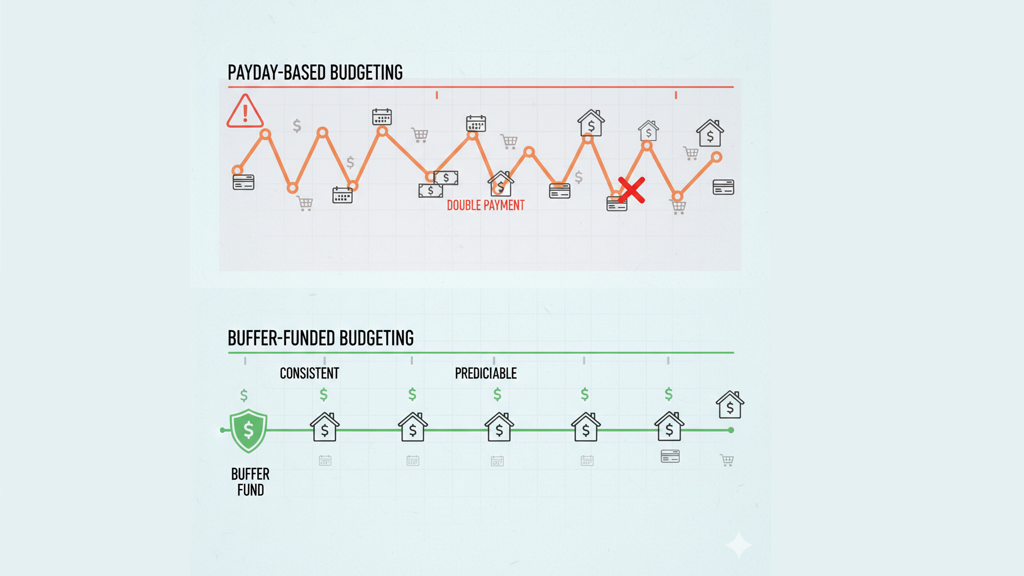

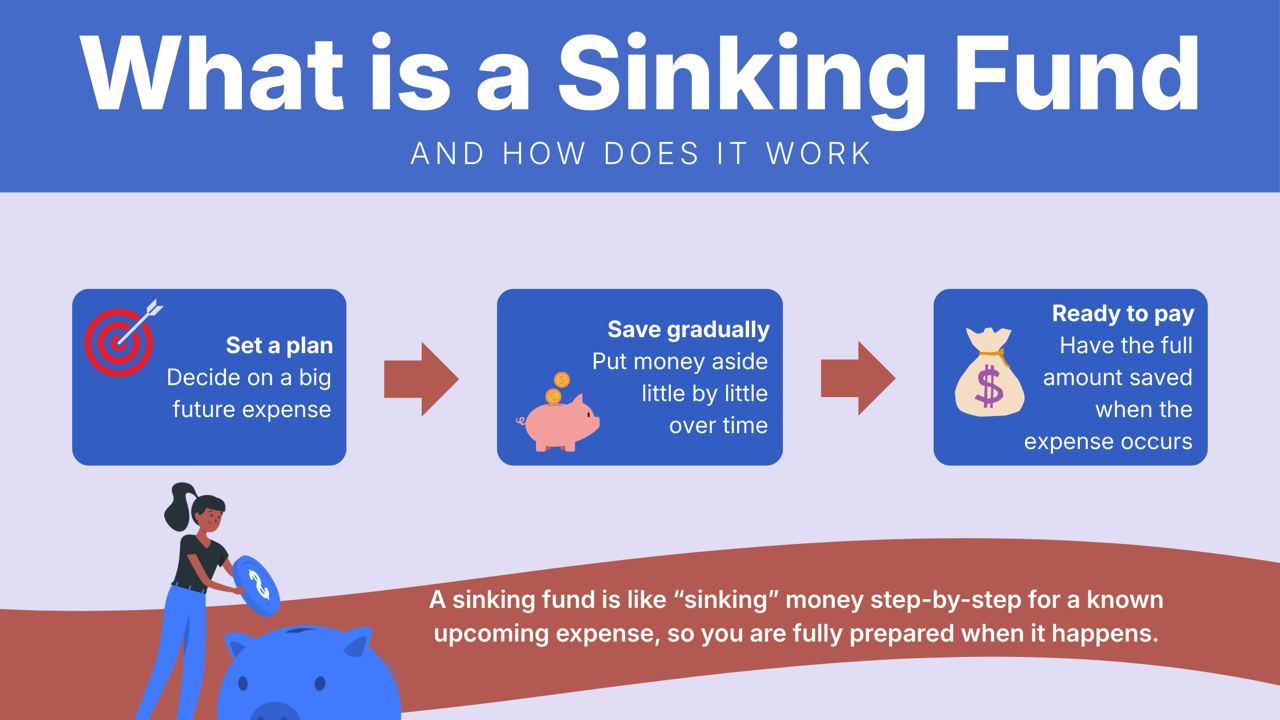

First Priority: Critical savings (emergency fund, investments, essential sinking funds)

Second Priority: The month itself (bills, groceries, living expenses)

Third Priority: Fun savings (trips, celebrations, wish-list stuff)

The rule: Total savings must hit ≥20% of combined income, but the critical stuff gets funded first, every single time.

What changed?

Less stress. Easier planning. And most importantly: I feel secure. I know the foundation is solid before we think about the vacation.

Why this works

PYF works because it removes willpower from the equation. You’re not deciding whether to save each month. You’re not hoping there’s money left over. You’re not fighting your impulses.

You’ve already paid yourself. The rest is just managing what remains.

The tiered approach works because it acknowledges reality: Not all financial goals have the same urgency. Your emergency fund matters more than your Christmas budget. Retirement matters more than a new TV.

How to start

1. Plan your priority savings first

At the beginning of each month, decide what’s critical: emergency fund, investments, down payments, sinking funds (insurance, car maintenance, annual expenses). These are non-negotiable.

2. Pay yourself first when the month begins

Transfer those priority savings immediately. First day of the month. Before anything else. These funds are now protected.

3. Live the month

Pay your bills, buy groceries, handle your needs and wants with what remains. This is your 50/30/20 framework in action.

4. Sweep the surplus into fun savings

Whatever’s left at month’s end? That goes to your flexible goals - personal spending money, vacation fund, Christmas budget, wish-list items.

The rule: Your total savings (priority + fun) should hit at least 20% of your combined income.

That’s it. Critical savings are guaranteed. Fun savings grow when you have good months. And you’ve just reversed your entire financial trajectory.

This is the foundation of how we built Monnetta - a budgeting app that makes this process visual and collaborative for couples and families. We spent 6 years perfecting this approach in spreadsheets before turning it into an app.

Have you tried Pay Yourself First? What worked (or didn’t work) for you?