· Guide · ![]() Rali · 5 min read

Rali · 5 min read

Sinking Funds - Your Budget’s Superpower

A practical approach to turning irregular expenses into planned, stress-free savings.

Ever had your car need new tires the same month your annual insurance bill hits? Or watched December arrive with holiday expenses piling up while you wonder where the money will come from? You’re not alone—and there’s a simple budgeting strategy that can eliminate this stress entirely.

The solution is called a sinking fund, and it’s one of the most underrated tools in personal finance. Let’s break down what it is, why it works, and how you can start using it today.

What is a Sinking Fund?

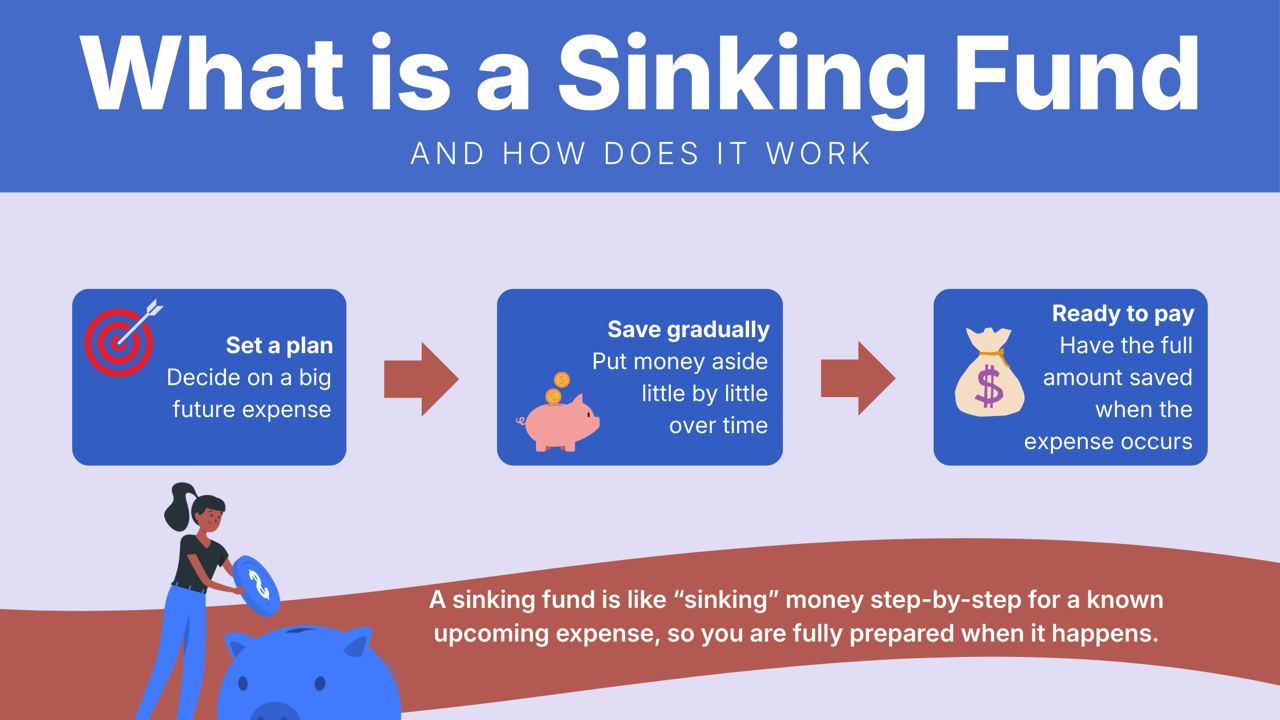

A sinking fund is money set aside for planned expenses that don’t happen monthly. Think of it as a dedicated savings account for specific, predictable costs.

Here’s the key distinction: It’s not an emergency fund. Your emergency fund covers things you can’t predict, like a job loss, urgent medical bills, and unexpected home repairs. A sinking fund handles expenses you know are coming, even if you don’t know exactly when, or simply don’t want to feel the financial sting all at once.

Instead of a big expense taking you by surprise, you save a small amount each month. And when the expense arrives, you’re ready — calm, prepared, and in control.

Sinking Funds vs. Emergency Funds

| Feature | Emergency Fund | Sinking Fund |

|---|---|---|

| Purpose | Unpredictable emergencies | Predictable, irregular expenses |

| Examples | Job loss, medical crisis | Car tyres, home maintenance, vet visits |

| Usage | Should rarely be touched | Used regularly for planned expenses |

New tires? Not an emergency—cars need tires.

Vet visit? Not an emergency if you have a pet.

When sinking funds handle predictable expenses, your emergency fund can focus on its real purpose: protecting you from genuine crises.

Top 3 Reasons - Why Sinking Funds Are Essential

- Avoid debt and stress – You become your own bank. Instead of paying a credit card company interest to borrow money, you’re paying yourself in advance.

- Guilt-Free Spending – When you use money from a sinking fund, you’re not ‘breaking the budget.’ The money was literally born for this purpose. And the feeling is great!

- Protect your future goals – Without sinking funds, when a big expense hits, people usually rob their retirement savings or dip into their “real” Emergency Fund. Sinking funds act as a buffer that keeps your long-term financial goals safe from short-term needs.

Plus, watching your sinking funds grow (even a little each month) gives a sense of achievement. It’s motivating to see tangible progress toward important goals, and that encourages you to keep going.

Common Sinking Fund Categories

Not sure where to start? Here are some of the most common sinking fund categories people find helpful:

- Car maintenance & repairs

- Annual insurance premiums

- Holiday and birthday gifts

- Tech replacements (phone, laptop)

- Pet care and vet visits

- Taxes and government fees

- Vacations

Pro-Tip: Many people keep their sinking funds in separate “sub-accounts” at their bank so they don’t accidentally spend the “New Roof” money on a fancy dinner. This physical separation provides clarity and discipline.

But managing multiple bank accounts can get complicated. That’s where tools like Monnetta come in.

How Monnetta Simplifies Sinking Funds

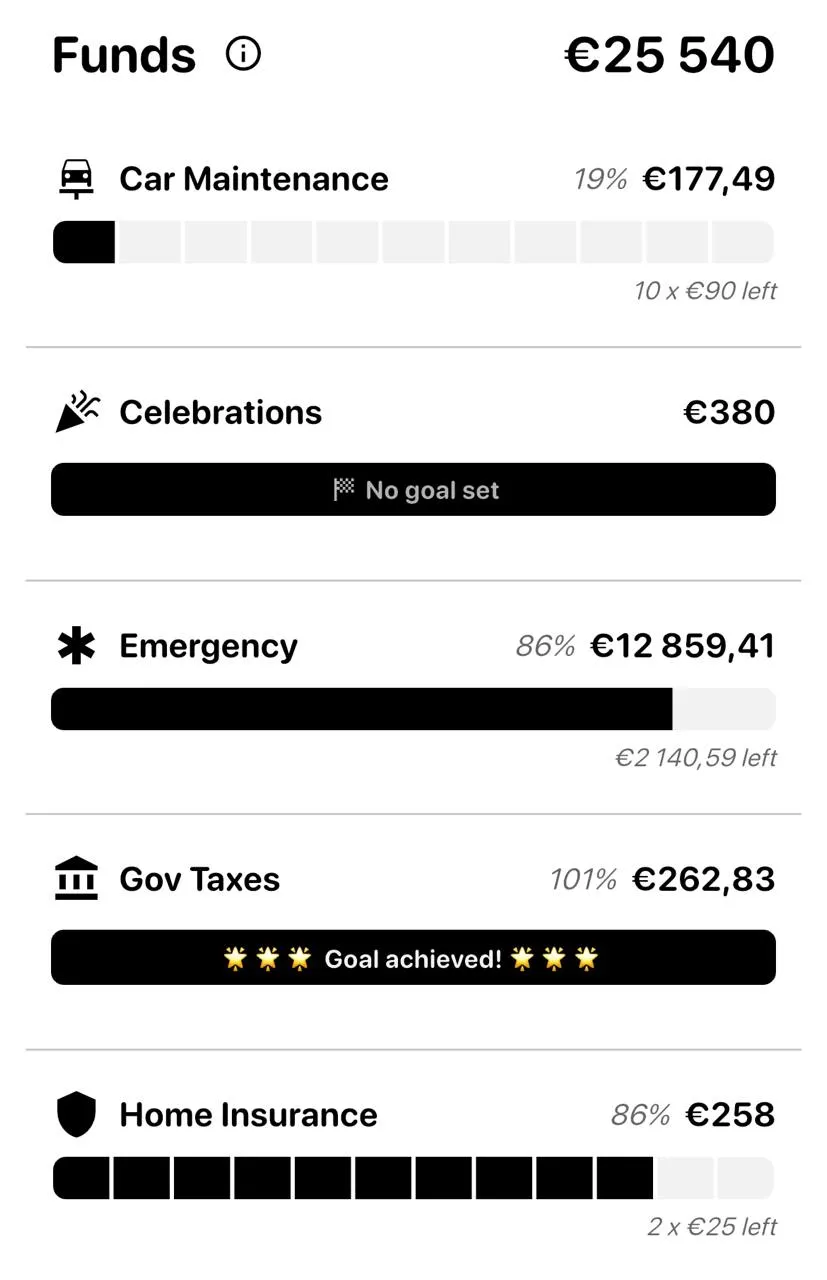

In Monnetta, we created a feature called Funds, a dedicated space where you can track all your funds and savings goals in one place.

Here’s what makes it powerful: you don’t need to create physical bank accounts or sub-accounts. Your money can stay in one place, but Monnetta helps you visualize and manage it in separate ‘digital pockets,’ each with its own purpose.

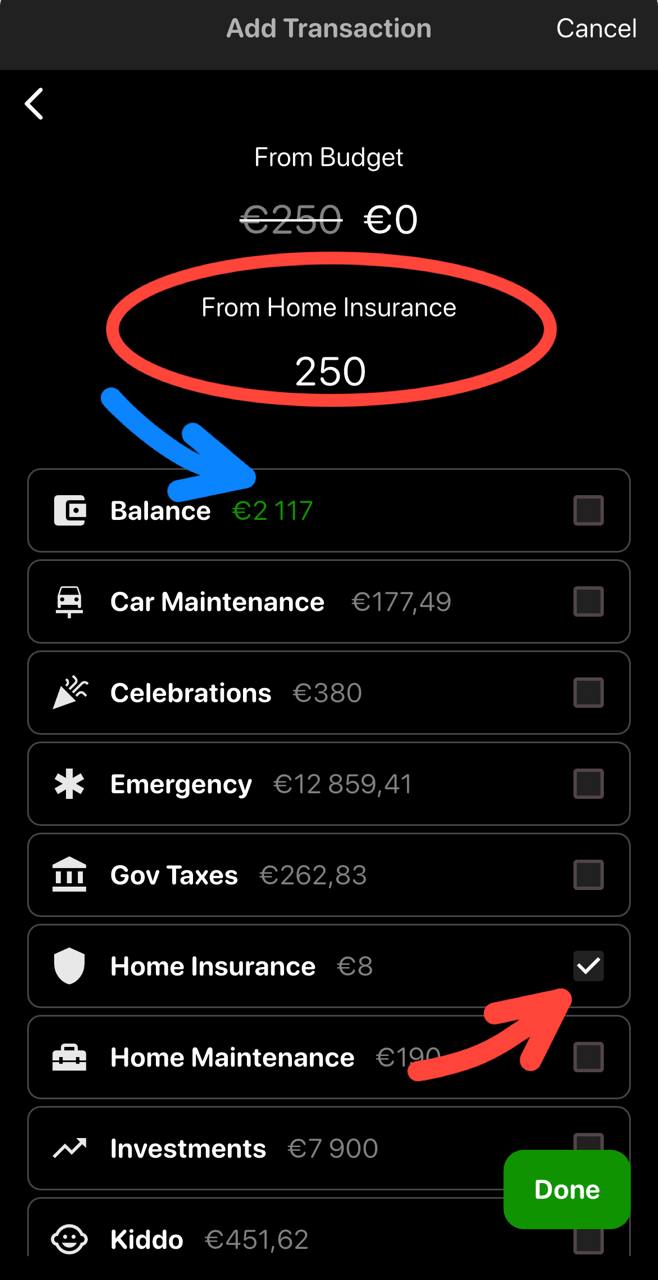

When an expense occurs, you can record the transaction in the current month while pulling the money from the appropriate fund—not from your daily spending. This way:

- The expense appears in your monthly statistics (so you maintain accurate records)

- Your daily budget isn’t impacted (because you’ve been saving for this all along)

For example, when your annual home insurance bill arrives, you log it in February’s expenses but mark the source as your ‘Home Insurance Fund.’ The transaction shows up in your February records, but your February budget remains intact because the money came from savings you’ve been building all year.

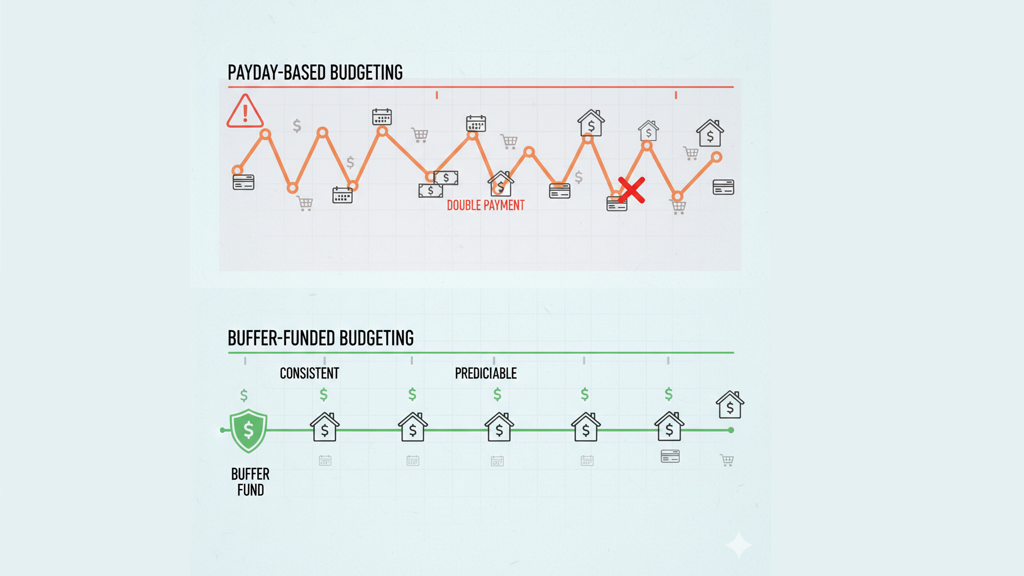

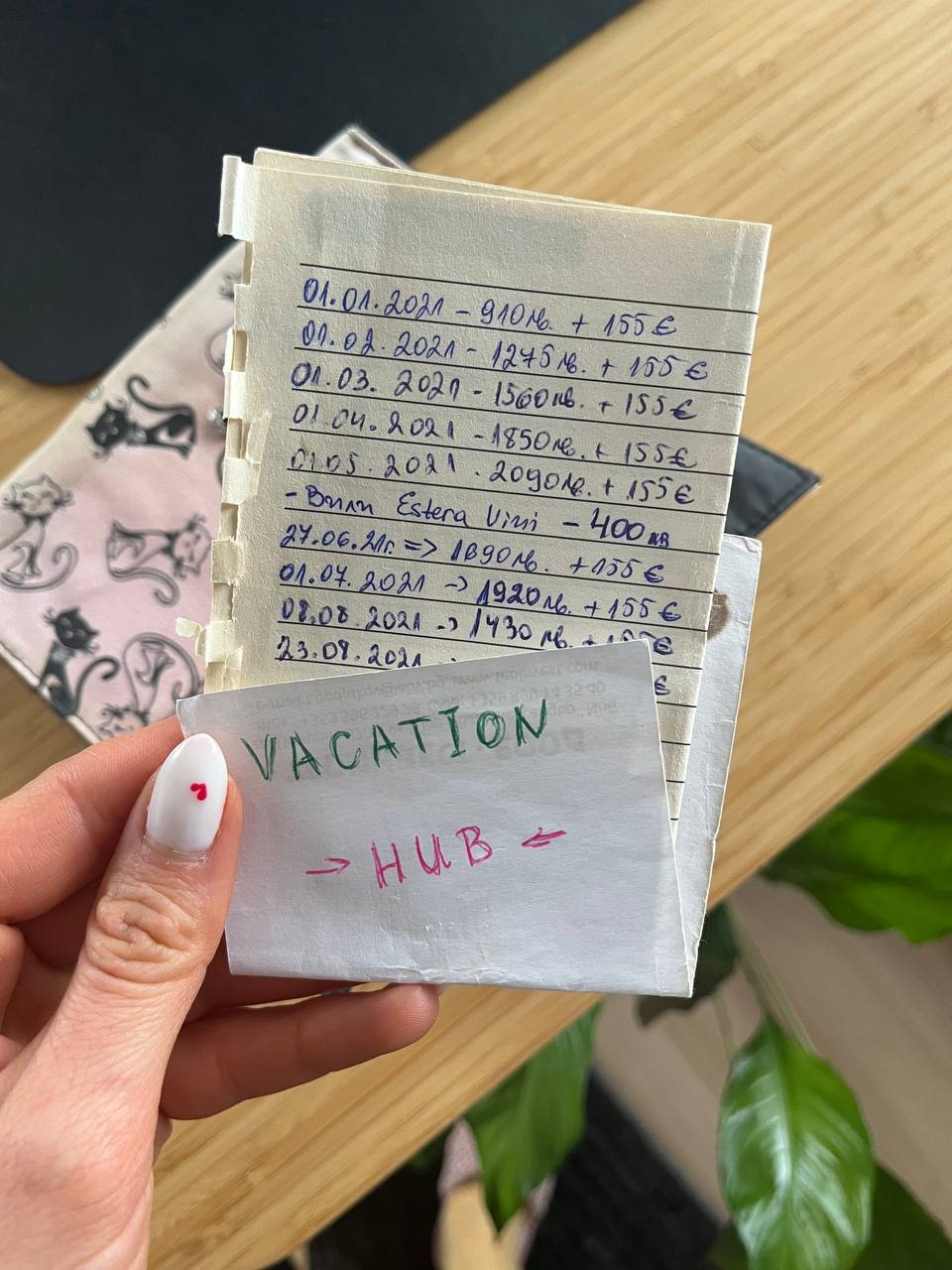

Below is our “before Monnetta” way of managing our Sinking Funds 😄

Fun Fact:

Why Is It Called “Sinking”?

It actually comes from old-school finance and government debt management from the 1700s.

It sounds a bit gloomy, right? Like a ship going down. But the term comes from the idea of “sinking” a debt. In the old days, companies would set aside money to gradually “sink” (pay off) a large debt so it didn’t crush them all at once.

Today, we use the same strategy to sink the cost of life’s big moments before they happen. Pretty cool that we’re still using a 300-year-old financial strategy!

Getting Started with Sinking Funds

Ready to create your first sinking fund? Here’s a simple approach:

1. Identify your irregular expenses.

Look back at the past year. What large, non-monthly expenses hit you? Write them down.

2. Calculate monthly contributions.

If your annual car insurance costs $1,200, you need to save $100 per month. Break down each expense into monthly amounts.

3. Start small.

You don’t need to fund everything at once. Pick 2–3 categories that cause you the most stress and start there. You can always add more funds as you get comfortable with the system.

4. Track consistently.

Whether you use separate bank accounts, a spreadsheet, or an app like Monnetta, the key is visibility. You need to see your progress and know where your money is allocated.

Final Thoughts

Sinking funds aren’t complicated, but they’re transformative. They turn financial anxiety into financial confidence. They replace scrambling with planning. They let you spend money on important things without guilt or stress.

Most importantly, they protect your emergency fund and long-term savings from being raided by predictable expenses disguised as surprises.

Start with just one or two categories. Build the habit. Watch the stress melt away. Your future self will thank you.